.avif)

DTI vs Residual Income Explained: A Deep California Mortgage Analysis You Shouldn’t Skip

When applying for a mortgage in California, most buyers hear about debt to income ratio. But if you are using a VA loan, another factor often carries more weight: residual income. Understanding the difference between these two can directly impact whether you get approved and how much you can borrow.

This detailed breakdown explains how DTI and residual income work, how lenders use them in 2026, and why California borrowers need to understand both before applying.

What Is Debt to Income Ratio (DTI)

DTI measures how much of your monthly income is used to pay debts.

Basic concept:

DTI = Total monthly debt ÷ Gross monthly income

Example:

- Monthly income: 8,000

- Total debts: 3,200

- DTI: 40 percent

What counts in DTI:

- Mortgage payment

- Credit cards

- Auto loans

- Student loans

- Personal loans

DTI is expressed as a percentage and is widely used in FHA, conventional, and VA underwriting.

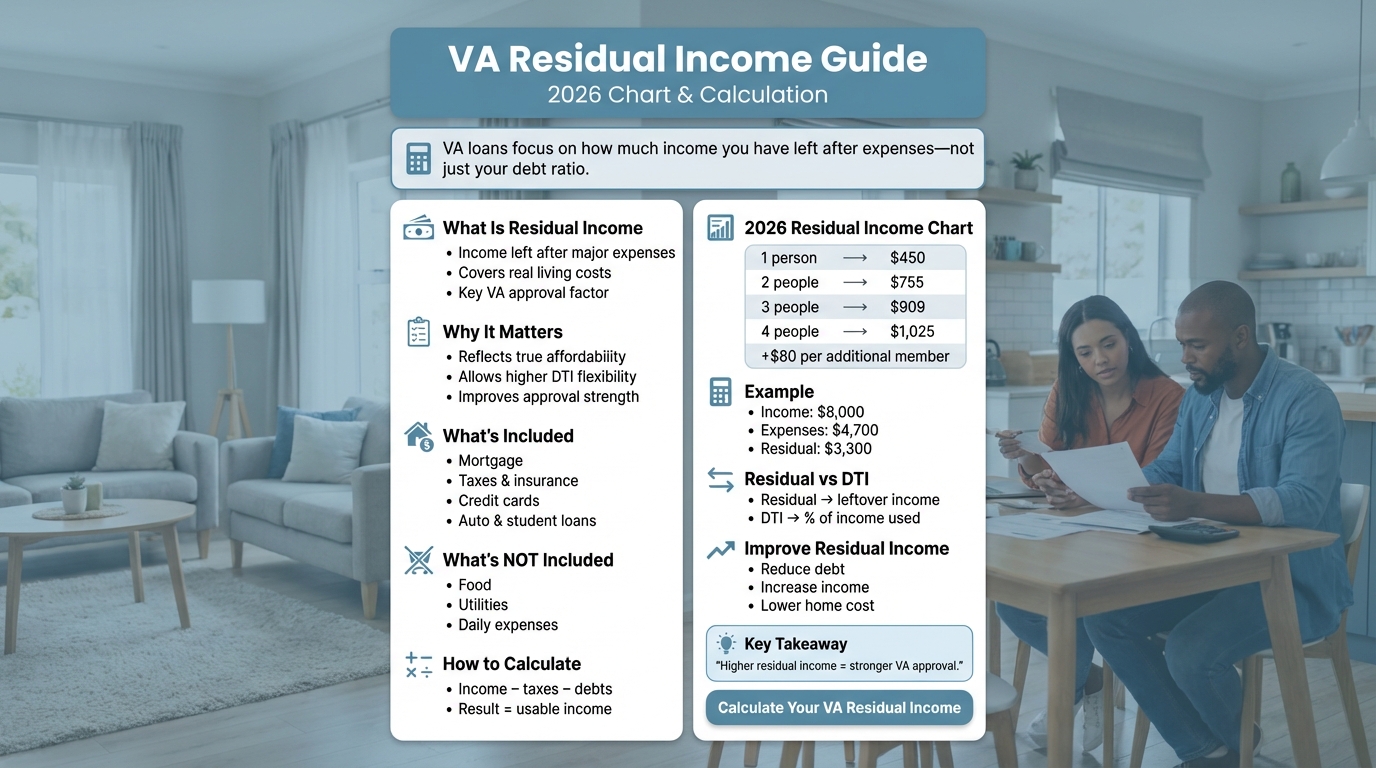

What Is Residual Income

Residual income measures how much money you have left after paying your obligations.

Basic concept:

Residual income = Income − taxes − debts − housing costs

Example:

- Income: 8,000

- Taxes: 1,500

- Debts and housing: 3,200

- Residual income: 3,300

This is the amount available for daily living expenses.

DTI vs Residual Income: Key Differences

Key takeaway:

DTI shows how much you owe, while residual income shows how much you actually have left.

Why VA Loans Prioritize Residual Income

VA loans focus on residual income because it reflects real affordability.

Why it matters:

- Accounts for cost of living

- Measures financial stability

- Reduces default risk

A borrower with a higher DTI may still qualify if their residual income is strong.

California Mortgage Reality: Why This Comparison Matters

California is a high cost state, which changes how these metrics behave.

Key challenges:

- Higher home prices

- Larger loan amounts

- Higher monthly payments

Result:

- DTI often looks higher

- Residual income becomes more important

This is why VA loans are especially valuable in California.

Typical DTI Guidelines in 2026

VA loans allow higher DTI if residual income is strong.

Residual Income Requirements (California Example)

These thresholds must be met after all major expenses.

Real World Scenario Comparison

Borrower A:

- Income: 9,000

- Debts: 4,000

- DTI: 44 percent

- Residual income: 3,000

Borrower B:

- Income: 9,000

- Debts: 3,000

- DTI: 33 percent

- Residual income: 1,200

Analysis:

- Borrower A has higher DTI but stronger residual income

- Borrower B has lower DTI but less financial cushion

In a VA loan scenario, Borrower A may be considered stronger.

When DTI Matters More

DTI plays a bigger role in:

- FHA loans

- Conventional loans

- Borrowers with limited income

- High debt scenarios

Lenders use DTI to assess basic risk levels.

When Residual Income Matters More

Residual income becomes critical in:

- VA loan approvals

- High cost states like California

- Larger households

- Borrowers with variable income

It provides a clearer picture of financial sustainability.

Pros and Cons of Each Metric

DTI Advantages:

- Simple to calculate

- Standard across all loan types

- Easy to compare borrowers

DTI Limitations:

- Does not account for cost of living

- Ignores remaining income

- Can misrepresent affordability

Residual Income Advantages:

- Reflects real financial capacity

- Accounts for expenses beyond debt

- More accurate in high cost areas

Residual Income Limitations:

- More complex to calculate

- Not used in all loan programs

How to Improve Both DTI and Residual Income

Improve DTI:

- Pay down existing debt

- Avoid new credit

- Increase income

Improve Residual Income:

- Reduce monthly obligations

- Choose a lower home price

- Increase income sources

Both metrics can be improved with smart financial planning.

Biggest Mistake California Buyers Make

Many buyers focus only on DTI.

Reality:

- A low DTI does not guarantee approval

- Strong residual income can outweigh higher DTI

Ignoring residual income can lead to incorrect assumptions about eligibility.

Smart Strategy for 2026 Buyers

- Check both DTI and residual income before applying

- Use residual income as your true affordability benchmark

- Do not rely only on lender prequalification

Final Insight

DTI and residual income measure two different aspects of your financial health. In California, where costs are higher, residual income often provides a more accurate picture of whether you can afford a home.

For VA borrowers, residual income is not just important. It is often the deciding factor. Understanding both metrics gives you a clear advantage when navigating the mortgage process in 2026.

FAQs

1. What is the difference between DTI and residual income

DTI measures how much income goes toward debt, while residual income measures how much money you have left after expenses.

2. Which is more important for VA loans

Residual income is more important because it reflects real affordability.

3. Can I qualify with high DTI

Yes, especially with a VA loan if your residual income is strong.

4. What is a good residual income level

It depends on family size and region, but higher amounts improve approval chances.

5. Why is residual income important in California

Because of higher living costs, it provides a more realistic measure of affordability.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)