.avif)

Fully Indexed Rate Explained: The Number That Ultimately Determines Many ARM Payments in South Carolina

Many South Carolina homebuyers focus on the introductory interest rate when considering an Adjustable Rate Mortgage (ARM). While the initial rate can significantly impact early monthly payments, it is not the number that determines future adjustments. The figure that often matters most over the life of the loan is the fully indexed rate.

Understanding the fully indexed rate can help borrowers evaluate future payment changes, compare ARM options more effectively, and make informed mortgage decisions. Whether you are purchasing a home in Charleston, Columbia, Greenville, Myrtle Beach, or elsewhere in South Carolina, knowing how ARM rates work is essential before signing loan documents.

What Is a Fully Indexed Rate?

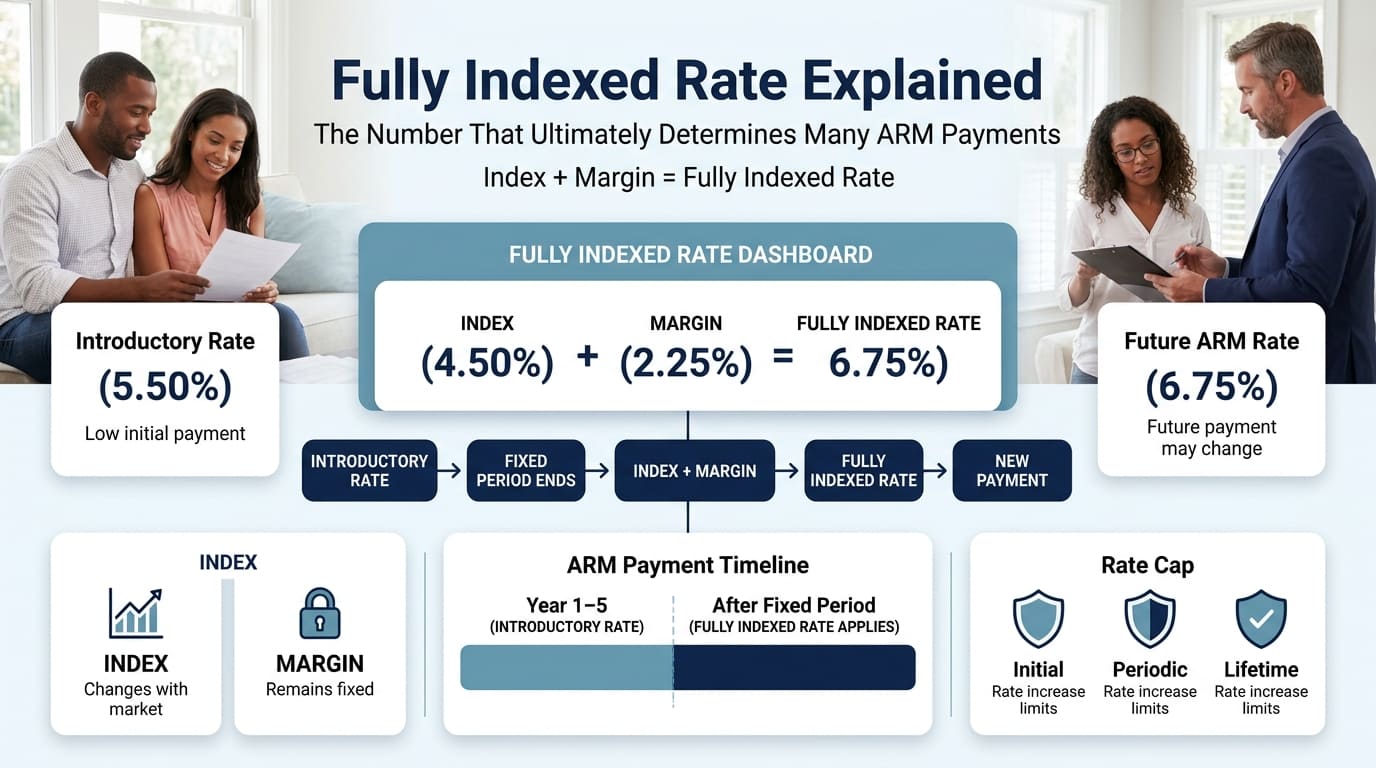

A fully indexed rate is the interest rate an adjustable rate mortgage uses after combining the loan's index and margin.

This rate determines what borrowers may pay once the introductory fixed period ends.

Fully Indexed Rate Formula

Index + Margin = Fully Indexed Rate

While introductory ARM rates may be discounted during the initial fixed period, future rate adjustments are generally based on this formula.

Example

In this example, the fully indexed rate equals 6.75%.

Key Takeaway

The fully indexed rate is often the interest rate used to determine future ARM adjustments after the introductory period expires.

Why Does the Fully Indexed Rate Matter?

Many borrowers focus solely on the initial ARM rate.

However, the introductory rate eventually expires.

Once that happens, future payments may be influenced by the fully indexed rate and any applicable rate adjustment caps.

Understanding this number helps borrowers evaluate:

- Future payment scenarios

- Long term affordability

- Interest rate risk

- ARM versus fixed rate comparisons

A low introductory rate does not necessarily indicate a low future payment.

What Determines the Fully Indexed Rate?

One of the most common borrower questions is: What determines the fully indexed rate?

The answer involves two components.

The Index

The index is a benchmark interest rate that fluctuates based on broader market conditions.

Common mortgage indexes may include:

- SOFR based indexes

- Treasury related benchmarks

- Other approved market indexes

The index changes over time.

The Margin

The margin is a fixed percentage established by the lender when the loan originates.

Unlike the index, the margin generally remains constant throughout the loan's life.

Fully Indexed Rate Calculation

Key Takeaway

The index moves with market conditions while the margin remains fixed. Together they determine the fully indexed rate.

How to Calculate Fully Indexed Rate

Many borrowers ask: How to calculate fully indexed rate?

The calculation is straightforward.

Formula

Current Index + Loan Margin = Fully Indexed Rate

Example One

Example Two

As market indexes increase or decrease, the fully indexed rate may change accordingly.

Pro Tip

Always ask your lender for both the current index and the loan margin before choosing an ARM. Looking only at the introductory rate may not provide a complete picture of future payment potential.

How Fully Indexed Rates Affect ARM Payments

The fully indexed rate plays a major role in determining future monthly payments.

When the fixed period ends:

- The loan reviews the current index

- The margin is added

- Adjustment caps are applied

- The new payment is calculated

This process repeats according to the loan's adjustment schedule.

Example

A borrower obtains a 5/6 ARM with an introductory rate of 5.50%.

Five years later:

- Index = 4.75%

- Margin = 2.25%

- Fully Indexed Rate = 7.00%

The payment adjustment may be based on this rate, subject to any periodic or lifetime caps.

Understanding Rate Caps

The fully indexed rate is important, but ARM borrowers should also understand adjustment caps.

Rate caps help limit how much interest rates can increase.

Common ARM Caps

These caps can reduce the impact of rapidly rising interest rates.

Key Takeaway

The fully indexed rate helps determine the target rate, but adjustment caps may limit how quickly the mortgage rate can reach that level.

Why South Carolina Borrowers Should Pay Attention

South Carolina continues to attract buyers relocating from higher cost states.

Many borrowers consider ARMs because they often provide lower initial rates than fixed rate mortgages.

Common situations include:

- First time homebuyers

- Relocating professionals

- Military families

- Buyers planning shorter ownership periods

Understanding future payment possibilities helps borrowers avoid surprises after the fixed period expires.

Example

A buyer moving to Charleston may expect to relocate again within seven years.

An ARM could potentially offer savings during the planned ownership period.

However, understanding the fully indexed rate remains important if plans change and the property is held longer.

ARM Versus Fixed Rate Mortgage

Borrowers often compare adjustable rate mortgages with fixed rate options.

ARM Advantages

- Lower initial rates

- Potential early payment savings

- Useful for shorter ownership timelines

Fixed Rate Advantages

- Stable monthly payments

- Predictable long term budgeting

- Protection from future rate increases

The right choice depends on financial goals, risk tolerance, and expected ownership duration.

Common Misconceptions About Fully Indexed Rates

Myth: The Introductory Rate Lasts Forever

False.

ARM rates eventually adjust according to loan terms.

Myth: The Margin Changes Every Year

False.

The margin generally remains fixed after loan origination.

Myth: Fully Indexed Rate Guarantees Future Payments

Not always.

Adjustment caps may influence the actual rate applied.

Myth: ARM Borrowers Never Benefit

False.

Many borrowers successfully use ARMs when their financial plans align with the loan structure.

Key Factors That Influence Future ARM Payments

Key Takeaway

The fully indexed rate is one of the most important numbers ARM borrowers should understand before selecting an adjustable rate mortgage.

Why Understanding Fully Indexed Rates Can Save Borrowers Money

Borrowers often become attracted to the lowest advertised rate without evaluating long term implications.

A strong mortgage decision requires understanding:

- Initial rate

- Fully indexed rate

- Margin

- Adjustment schedule

- Rate caps

Reviewing these factors provides a clearer picture of future affordability.

Why I Believe Many ARM Borrowers Focus on the Wrong Number

After helping borrowers evaluate mortgage options, I have found that many focus exclusively on the introductory rate while overlooking the mechanics that drive future adjustments.

The introductory rate certainly matters. It affects affordability during the early years of the loan. However, borrowers who understand the fully indexed rate gain a much better understanding of what could happen after the fixed period expires.

The strongest mortgage decisions occur when buyers evaluate both today's payment and tomorrow's possibilities. Understanding how the fully indexed rate works allows borrowers to make decisions based on long term financial planning rather than short term marketing numbers.

For South Carolina buyers considering an ARM, that knowledge can make a significant difference.

— Bill Marshall

Ready to Explore ARM Options?

Platinum Capital Advisors helps South Carolina homebuyers evaluate adjustable rate mortgages, understand future payment scenarios, compare loan structures, and determine whether an ARM aligns with their financial goals.

Whether you are purchasing your first home or refinancing an existing property, understanding the fully indexed rate can help you make a more informed mortgage decision.

Frequently Asked Questions

What is a fully indexed rate?

A fully indexed rate is the interest rate created by adding the current index to the lender's margin. It often determines future ARM rate adjustments.

What determines the fully indexed rate?

The fully indexed rate is determined by two components: the current market index and the fixed margin established by the lender.

How to calculate fully indexed rate?

Calculate the fully indexed rate by adding the current index value to the loan's margin.

Does the margin change over time?

Typically no. The margin is generally fixed when the loan is originated.

Why is the fully indexed rate important?

It helps borrowers understand potential future ARM payments after the introductory fixed rate period ends.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)