.avif)

Before You Assume You’re Out of Benefits: See How Bonus Entitlement Actually Expands Your Limit in California

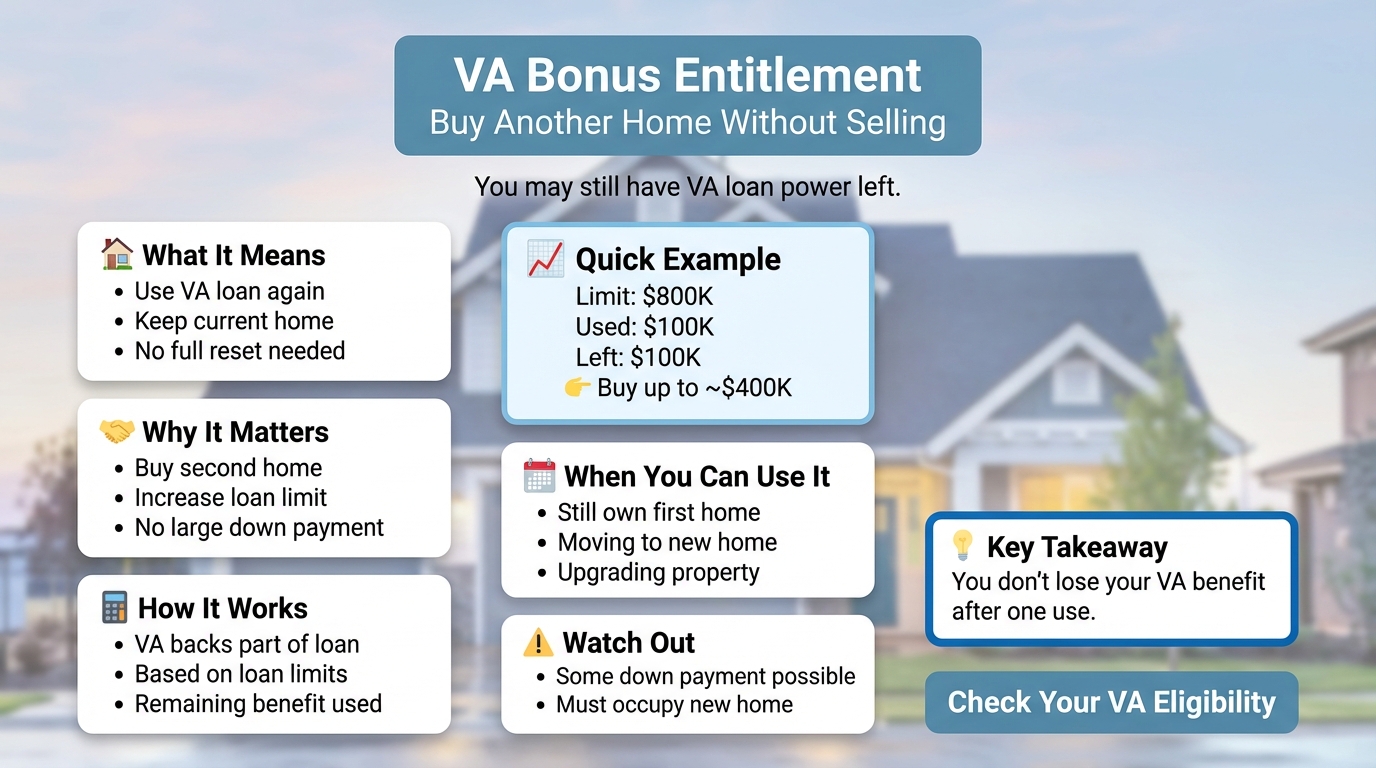

Many California veterans believe they have used up their VA loan benefit after purchasing one home. That assumption is often incorrect. The VA loan program includes something called bonus entitlement, which can significantly increase your borrowing power, even if you already have an active VA loan.

This guide explains what is bonus entitlement for VA loan, how it works, and how you can use it to buy again in California in 2026.

What Is Bonus Entitlement for VA Loan

Bonus entitlement, also known as second tier entitlement, is additional VA loan backing that allows eligible borrowers to:

- Purchase another home using a VA loan

- Buy a higher priced property without a down payment

- Keep an existing VA loan and still use remaining benefits

Key idea:

You do not lose your VA benefit after one use. It can be reused and expanded.

How VA Loan Entitlement Works

To understand va loan bonus entitlement, you need to know the two parts of entitlement.

1. Basic Entitlement

- Typically up to 36,000

- Covers smaller loan amounts

2. Bonus Entitlement

- Applies to larger loans

- Tied to conforming loan limits

- Expands your purchasing power

In high cost states like California, bonus entitlement plays a major role.

Why Bonus Entitlement Matters in California

California home prices are higher than the national average, which makes standard entitlement insufficient in many cases.

Key benefit:

Bonus entitlement allows you to buy homes above standard limits with little or no down payment.

VA Loan Limits and Bonus Entitlement (2026)

In 2026, VA loan limits align with conforming loan limits.

Example (approximate):

- Standard limit: around 766,000

- High cost California counties: can exceed 1,000,000

What this means:

If you have full entitlement, there is no official loan cap.

If you have partial entitlement, bonus entitlement determines how much more you can borrow.

How Bonus Entitlement Expands Your Buying Power

Let’s break down a simple example.

Scenario:

- You already used 200,000 of entitlement

- Remaining entitlement still available

- You want to buy another home

Result:

You can still purchase another property using the remaining entitlement, depending on loan limits.

VA Bonus Entitlement Calculation Explained

Understanding va bonus entitlement calculation helps you estimate your eligibility.

Basic formula concept:

Maximum VA guarantee = 25 percent of county loan limit

Remaining entitlement = Total entitlement − used entitlement

Maximum loan = Remaining entitlement × 4

Example:

This shows how your borrowing capacity is calculated.

VA Bonus Entitlement Worksheet Example

This format helps you visualize how much benefit you still have.

VA Bonus Entitlement Calculator Concept

A va bonus entitlement calculator works by:

- Identifying your county loan limit

- Subtracting used entitlement

- Calculating remaining eligibility

While exact numbers vary, the logic remains consistent.

When You Can Use Bonus Entitlement

You can use bonus entitlement in several situations.

Common scenarios:

- You still own your first home

- You want to buy a second home

- You previously used a VA loan but did not restore full entitlement

- You are purchasing in a higher price range

VA Bonus Entitlement vs Full Entitlement

Even if you do not have full entitlement, bonus entitlement still provides significant flexibility.

Advantages of VA Bonus Entitlement

Key benefits:

- Buy another home without selling your current one

- Increase loan size in high cost markets

- Avoid large down payments

- Continue using VA loan advantages

Limitations to Consider

Important factors:

- Remaining entitlement may limit loan size

- Down payment may be required in some cases

- Lender guidelines still apply

- Occupancy rules must be followed

Common Misconceptions

Myth:

You can only use a VA loan once

Reality:

You can use it multiple times through bonus entitlement

Myth:

You must sell your home to reuse VA benefits

Reality:

Bonus entitlement allows multiple uses without selling

California Example Scenario

Buyer profile:

- Owns current home with VA loan

- Wants to buy another home in California

- Has partial entitlement remaining

Outcome:

- Can still qualify for second VA loan

- Loan amount depends on remaining entitlement and county limits

How to Maximize Your VA Loan Benefit

Smart strategies:

- Understand your current entitlement usage

- Check county loan limits

- Work with lenders experienced in VA loans

- Consider restoring entitlement if possible

When You Should Consider Restoring Entitlement

Restoring entitlement may help if:

- You sold your previous home

- You paid off your VA loan

- You want full borrowing power again

Final Insight

Bonus entitlement is one of the most powerful and misunderstood features of the VA loan program. In California, where home prices are higher, it can significantly expand your ability to buy again or move up to a more expensive property.

Before assuming you are out of benefits, it is essential to understand how much entitlement you still have. In many cases, you have far more borrowing power than you think.

FAQs

1. What is bonus entitlement for VA loan

It is additional VA loan eligibility that allows you to borrow more or use your benefit again.

2. Can I use a VA loan twice

Yes, bonus entitlement allows multiple uses depending on remaining eligibility.

3. How is VA bonus entitlement calculated

It is based on county loan limits and how much entitlement you have already used.

4. Do I need a down payment with bonus entitlement

Not always, but it depends on your remaining entitlement and loan size.

5. Can I have two VA loans at the same time

Yes, in certain situations if you have enough remaining entitlement.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)