.avif)

VA DTI Limits 2026: Why Some California Veterans Qualify Above Traditional Debt Ratio Thresholds

For many California veterans, one of the biggest misconceptions about qualifying for a VA loan is believing there is a strict debt to income cap that automatically disqualifies them. In reality, VA DTI limits are more flexible than many conventional mortgage guidelines. In 2026, qualified veterans may still receive approval even when their debt ratios exceed traditional lending thresholds.

Understanding how VA DTI limits work can help veterans make informed home financing decisions and avoid eliminating themselves from consideration before speaking with a lender.

What Are VA DTI Limits?

Debt to income ratio, commonly called DTI, measures how much of your gross monthly income goes toward debt obligations. Lenders use this calculation to determine whether you can comfortably manage a new mortgage payment alongside your existing financial commitments.

The basic formula is:

Total Monthly Debt Payments ÷ Gross Monthly Income = Debt to Income Ratio

For example:

If monthly gross income equals $8,000:

$3,500 ÷ $8,000 = 43.75% DTI

Many borrowers assume this percentage creates a hard approval limit. With VA financing, that is often not the case.

Why VA DTI Limits Are Different

Unlike many conventional mortgage programs, the Department of Veterans Affairs does not establish a strict maximum debt ratio that applies to every borrower.

Instead, VA underwriting evaluates the complete financial profile of the veteran.

Lenders look beyond a simple percentage and consider:

- Residual income

- Credit history

- Employment stability

- Cash reserves

- Overall financial strength

- Property occupancy requirements

Because of this approach, veterans with higher debt ratios may still qualify when other compensating factors exist.

Key Takeaway

VA loans are designed to evaluate overall affordability rather than relying exclusively on a fixed debt ratio threshold.

VA DTI Limits 2026 Overview

While VA guidelines remain flexible, lenders generally use certain benchmarks during the underwriting process.

Many California veterans are surprised to learn approvals can occur above 41% when other aspects of the application demonstrate financial stability.

The key factor is understanding how VA underwriting evaluates risk differently than many traditional loan programs.

Why California Veterans Often Qualify Above Traditional Thresholds

California housing markets create unique affordability challenges.

Home prices throughout regions such as:

- Los Angeles County

- Orange County

- San Diego County

- Riverside County

- Sacramento County

often require larger mortgage payments compared to many parts of the country.

To address these realities, VA underwriting places significant emphasis on residual income calculations rather than relying solely on debt ratios.

Residual Income Matters More

Residual income measures how much money remains after:

- Housing expenses

- Taxes

- Existing debts

- Estimated household obligations

are deducted from monthly income.

This remaining income demonstrates the borrower's ability to handle everyday living expenses.

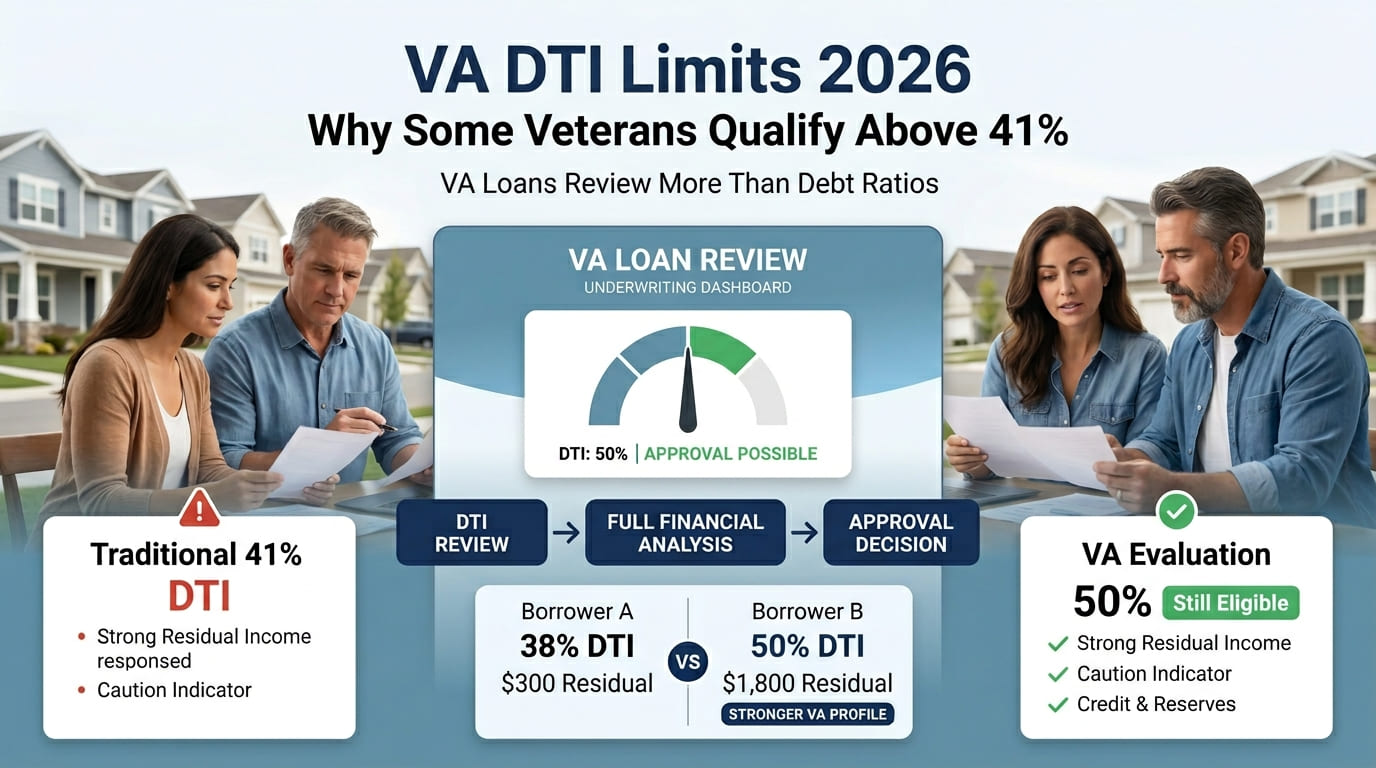

A veteran with a 50% DTI and substantial residual income may present less risk than a borrower with a 38% DTI and very little remaining monthly cash flow.

Example

Borrower A:

- 38% DTI

- $300 residual income

Borrower B:

- 50% DTI

- $1,800 residual income

Under VA analysis, Borrower B may actually represent the stronger financial profile.

Compensating Factors That Can Support Higher VA DTI Limits

Several factors can strengthen a VA loan application when debt ratios exceed traditional benchmarks.

Strong Credit Scores

Higher credit scores demonstrate responsible financial management.

Veterans with scores above 720 frequently receive more favorable underwriting consideration than applicants with lower scores.

Significant Cash Reserves

Savings remaining after closing provide an additional safety cushion.

Lenders view reserve funds as evidence that unexpected expenses can be managed without financial hardship.

Stable Employment History

Long term employment within the same industry can reduce perceived lending risk.

Consistent income often offsets concerns associated with elevated debt ratios.

Minimal Payment Shock

If the proposed mortgage payment closely resembles current housing expenses, lenders may view the transaction more favorably.

High Residual Income

This remains one of the strongest compensating factors available under VA financing.

Pro Tip

Veterans concerned about debt ratios should focus on improving overall financial strength rather than concentrating solely on one percentage calculation.

Common Debts Included in VA DTI Calculations

Understanding what counts toward debt ratios helps borrowers prepare before applying.

Most lenders include:

- Mortgage payment

- Property taxes

- Homeowners insurance

- HOA dues

- Auto loans

- Student loans

- Personal loans

- Minimum credit card payments

- Child support obligations

- Alimony payments

These obligations collectively determine the debt ratio used during underwriting.

How Veterans Can Improve Approval Chances

Even though VA DTI limits offer flexibility, borrowers can strengthen their applications before applying.

Reduce Revolving Debt

Paying down credit card balances may improve both debt ratios and credit scores simultaneously.

Avoid New Financing

Opening new loans before applying can increase monthly obligations and reduce qualification capacity.

Build Emergency Savings

Additional reserves create stronger underwriting profiles.

Review Credit Reports

Correcting reporting errors can improve credit scores and overall approval potential.

Work With Experienced VA Loan Professionals

Understanding lender overlays and VA underwriting nuances often makes a significant difference in qualification outcomes.

Key Factors Underwriters Review Beyond DTI

Key Takeaway

VA underwriting evaluates the complete financial picture. Debt ratio is only one component of the approval process.

Why Some Veterans Are Declined Despite Flexible DTI Guidelines

Many denials occur because borrowers focus solely on debt ratios while overlooking other qualifying factors.

Common issues include:

- Insufficient residual income

- Recent late payments

- Unstable employment history

- Excessive revolving debt

- Limited cash reserves

Improving these areas often creates more meaningful results than attempting to lower DTI alone.

Why I Believe Many Veterans Misunderstand VA DTI Limits

After helping California veterans navigate the mortgage process, one pattern appears repeatedly. Many borrowers assume a debt ratio above 41% automatically ends their chances of approval.

That assumption causes qualified veterans to delay homeownership unnecessarily.

The strongest VA borrowers are not always those with the lowest debt ratios. They are often the borrowers with stable employment, strong residual income, responsible credit management, and a clear understanding of their financial capacity.

VA financing was designed to recognize the complete financial profile of the borrower. When veterans understand how the program actually works, they often discover opportunities that traditional lending guidelines would not provide.

— Bill Marshall

Ready to Explore Your VA Loan Options?

Platinum Capital Advisors helps California veterans understand their financing options and evaluate whether their financial profile meets current VA loan requirements.

Whether your debt ratio falls below traditional thresholds or exceeds common benchmarks, a complete qualification review can provide clarity and help identify the best path forward.

Frequently Asked Questions

What are the VA DTI limits in 2026?

There is no official maximum VA debt to income ratio. Many lenders use 41% as a benchmark, but approvals above that level are common when compensating factors exist.

Can I get a VA loan with a 50% debt ratio?

Yes. Many veterans receive approval above 50% when they demonstrate strong residual income, good credit, stable employment, and adequate reserves.

Does residual income matter more than DTI?

In many cases, yes. Residual income is a core component of VA underwriting and often carries significant weight during the approval process.

What debts count toward VA DTI calculations?

Mortgage payments, taxes, insurance, car loans, student loans, personal loans, credit card minimum payments, child support, and other recurring obligations are generally included.

Can California veterans qualify with higher debt ratios?

Yes. Because of California housing costs and VA underwriting flexibility, qualified veterans may receive approval above traditional debt ratio thresholds when overall financial strength is demonstrated.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)