.avif)

Why Some Georgia ARM Borrowers Benefit From Federal Reserve Rate Changes While Others Do Not

When news headlines announce that the Federal Reserve has raised or lowered interest rates, many Georgia homeowners immediately wonder how those changes will affect their mortgage payments. For borrowers with Adjustable Rate Mortgages (ARMs), the answer is not always straightforward.

Some ARM borrowers may see future payment changes influenced by broader interest rate movements, while others may experience little or no immediate impact. Understanding how Federal Reserve actions affect adjustable rate mortgages can help Georgia homeowners make more informed financing decisions.

Whether you live in Atlanta, Savannah, Augusta, Macon, Columbus, or elsewhere in Georgia, understanding the relationship between ARM loans and Federal Reserve policy is essential.

How the Federal Reserve Influences Mortgage Rates

The Federal Reserve does not directly set mortgage rates.

Instead, the Fed influences short term interest rates through monetary policy decisions.

These actions affect:

- Financial markets

- Banking costs

- Consumer lending rates

- Treasury yields

- Mortgage related indexes

Over time, many adjustable rate mortgage indexes respond to broader market conditions influenced by Federal Reserve policy.

Key Takeaway

The Federal Reserve does not directly control ARM rates, but its actions can influence the indexes used to calculate future mortgage adjustments.

What Is an Adjustable Rate Mortgage?

An Adjustable Rate Mortgage is a home loan that begins with a fixed interest rate for a specified period and later adjusts according to the loan's terms.

Common ARM products include:

- 5 Year ARM

- 7 Year ARM

- 10 Year ARM

During the fixed period:

- The interest rate remains unchanged

- Monthly principal and interest payments remain stable

After the fixed period ends:

- The interest rate may adjust periodically

- Monthly payments may increase or decrease

Why Some ARM Borrowers Benefit From Federal Reserve Rate Cuts

When the Federal Reserve lowers rates, market interest rates often decline over time.

For ARM borrowers whose loans are entering adjustment periods, lower indexes may result in lower future interest rates.

Example

A Georgia homeowner has a 7 Year ARM approaching its first adjustment.

If the applicable index decreases due to broader market conditions, the fully indexed rate may also decline.

Potential benefits include:

- Lower interest rate adjustments

- Reduced monthly payments

- Improved affordability

- Interest savings over time

Key Takeaway

ARM borrowers whose loans are actively adjusting may benefit when market indexes move lower.

Why Some ARM Borrowers Do Not Benefit

Many borrowers assume every Federal Reserve rate cut immediately lowers their mortgage payment.

That is not how ARM loans work.

Several factors determine whether a borrower actually benefits.

Fixed Period Still Active

Borrowers within the initial fixed p

For example:

Even if market rates decline, the introductory rate generally remains unchanged until the adjustment period begins.

Index Does Not Move Equally

The Federal Reserve influences markets, but ARM indexes do not always move in perfect alignment with Fed actions.

Indexes may:

- Increase

- Decrease

- Remain relatively stable

depending on broader economic conditions.

Adjustment Caps Apply

ARM loans often contain adjustment limits.

Even when indexes move significantly, caps may influence how much the rate changes during a specific adjustment period.

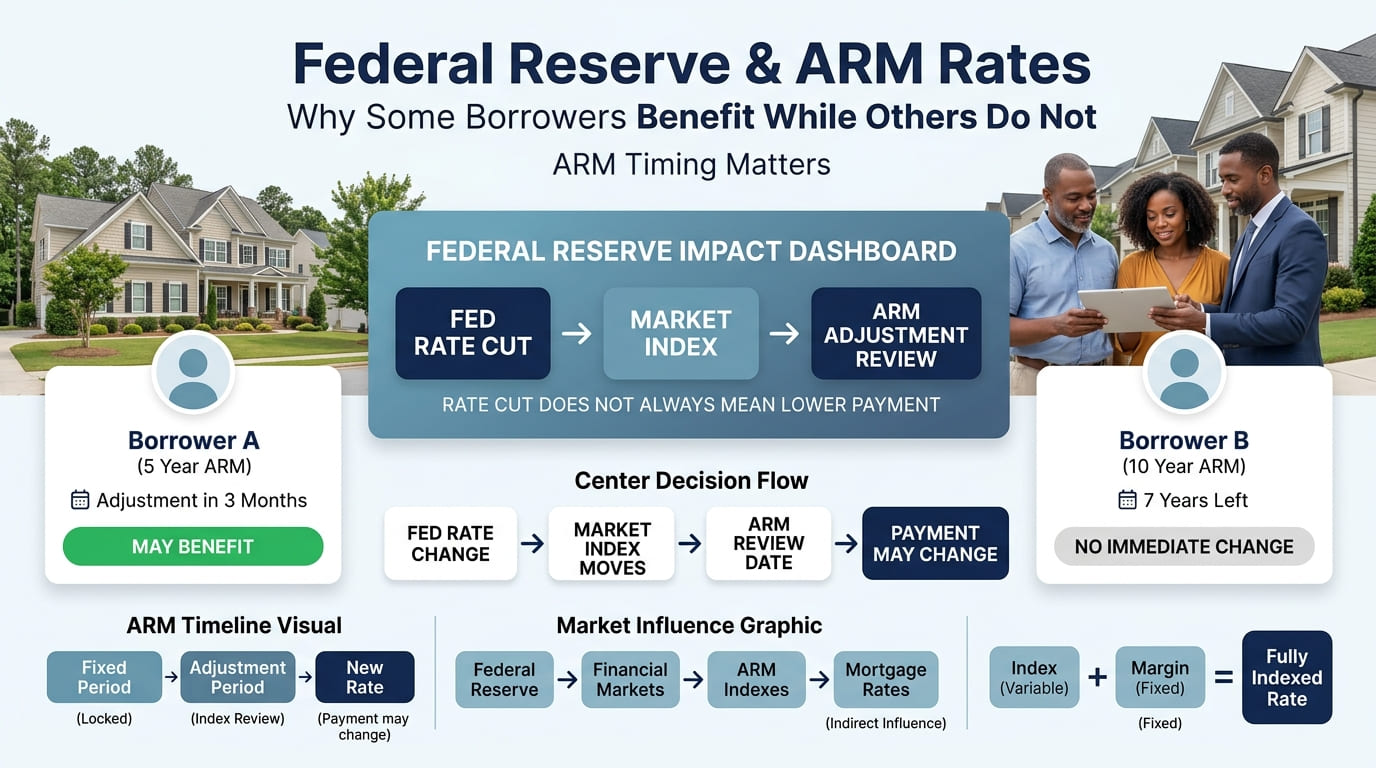

Understanding the ARM Adjustment Formula

Many borrowers mistakenly believe the Federal Reserve directly determines their mortgage rate.

In reality, most ARM adjustments rely on a formula involving an index and margin.

ARM Rate Formula

Index + Margin = Fully Indexed Rate

The index changes over time.

The margin generally remains fixed.

Example

When indexes move lower, future ARM adjustments may also decrease.

Pro Tip

Ask your lender which index your ARM uses and how frequently adjustments occur. Understanding these details provides a clearer picture of how future Federal Reserve actions may affect your loan.

Why Timing Matters for Georgia Borrowers

The timing of Federal Reserve decisions often determines whether borrowers see meaningful benefits.

Borrower A

- 10 Year ARM

- Fixed period has 7 years remaining

Federal Reserve cuts rates today.

Result:

No immediate payment change.

Borrower B

- 5 Year ARM

- First adjustment scheduled in three months

Federal Reserve cuts rates.

Result:

Potential benefit if the applicable index declines before the adjustment date.

Key Takeaway

Two borrowers can have identical ARM loans yet experience very different outcomes depending on where they are in the loan cycle.

Federal Reserve Rate Increases and ARM Borrowers

Federal Reserve rate hikes can create the opposite effect.

When market rates rise:

- Indexes may increase

- Future ARM adjustments may rise

- Monthly payments may increase

However, adjustment caps often provide some protection.

Common ARM Caps

These protections help reduce payment shock.

Why Georgia Borrowers Often Consider ARMs

Many Georgia buyers choose adjustable rate mortgages because they may offer lower initial rates compared to fixed rate options.

Common situations include:

- First time homebuyers

- Relocating professionals

- Military families

- Buyers planning shorter ownership periods

- Borrowers expecting future refinancing opportunities

For these borrowers, initial savings may outweigh long term rate uncertainty.

ARM Borrowers Most Likely to Benefit From Rate Changes

Certain borrowers are more likely to see benefits from declining market rates.

Borrowers Near Adjustment Dates

Loans approaching adjustment periods are more sensitive to current index levels.

Long Term ARM Holders

Homeowners planning to keep the mortgage beyond the fixed period may experience multiple adjustment cycles.

Borrowers Monitoring Refinance Opportunities

Lower rates may create refinancing opportunities in addition to ARM adjustment benefits.

Common Misconceptions About Federal Reserve Rate Changes

Myth: Every Rate Cut Lowers My Mortgage Payment

False.

Many borrowers remain within fixed periods.

Myth: ARM Rates Change Every Time the Fed Meets

False.

ARM adjustments occur according to the loan's adjustment schedule.

Myth: Federal Reserve Decisions Directly Set ARM Rates

False.

Mortgage indexes and broader market conditions ultimately influence ARM adjustments.

Myth: ARMs Always Become More Expensive

False.

ARM rates can move up or down depending on market conditions.

Key Factors That Determine ARM Payment Changes

Key Takeaway

Federal Reserve actions influence mortgage markets, but the structure of the ARM ultimately determines how those changes affect individual borrowers.

Why Understanding ARM Mechanics Matters

Many homeowners focus on economic headlines without fully understanding how their mortgage works.

A stronger approach involves understanding:

- Loan adjustment schedule

- Index used by the ARM

- Margin amount

- Adjustment caps

- Future payment scenarios

This knowledge helps borrowers evaluate opportunities and manage risk more effectively.

Why I Believe Many Borrowers Misunderstand Federal Reserve Impacts

After helping borrowers evaluate adjustable rate mortgages, I often find that many assume Federal Reserve announcements automatically change their mortgage payments.

In reality, the relationship is much more nuanced.

Some Georgia borrowers may benefit significantly from lower market rates if their loans are approaching adjustment periods. Others may see little immediate effect because their fixed period remains active for several years.

The borrowers who make the best decisions are those who understand both the broader economic environment and the specific structure of their mortgage. Federal Reserve policy matters, but understanding how your ARM actually works matters even more.

— Bill Marshall

Ready to Evaluate Your ARM Options?

Platinum Capital Advisors helps Georgia homebuyers and homeowners understand adjustable rate mortgages, payment adjustment risks, refinancing opportunities, and long term mortgage planning.

Whether you are considering an ARM or already have one, understanding how Federal Reserve rate changes interact with your loan structure can help you make informed financial decisions.

Frequently Asked Questions

Do Federal Reserve rate cuts automatically lower ARM payments?

No. ARM payments generally change according to the loan's adjustment schedule and the applicable index.

Why do some ARM borrowers benefit from rate cuts?

Borrowers approaching adjustment periods may benefit if lower market rates reduce the index used to calculate future adjustments.

Can ARM rates decrease?

Yes. If market indexes decline and loan terms allow, ARM rates may decrease during adjustment periods.

What determines ARM rate adjustments?

Most ARM adjustments are based on an index, a margin, adjustment caps, and the loan's adjustment schedule.

Are ARMs good for Georgia homebuyers?

ARMs may be beneficial for borrowers who expect shorter ownership periods or who understand and are comfortable with future rate adjustment risks.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)