.avif)

VA Loan Income Requirements in 2026: What Borrowers Need to Know

Many homebuyers believe they must earn a certain income to qualify for a mortgage. This assumption often creates confusion for veterans and service members exploring VA loans.

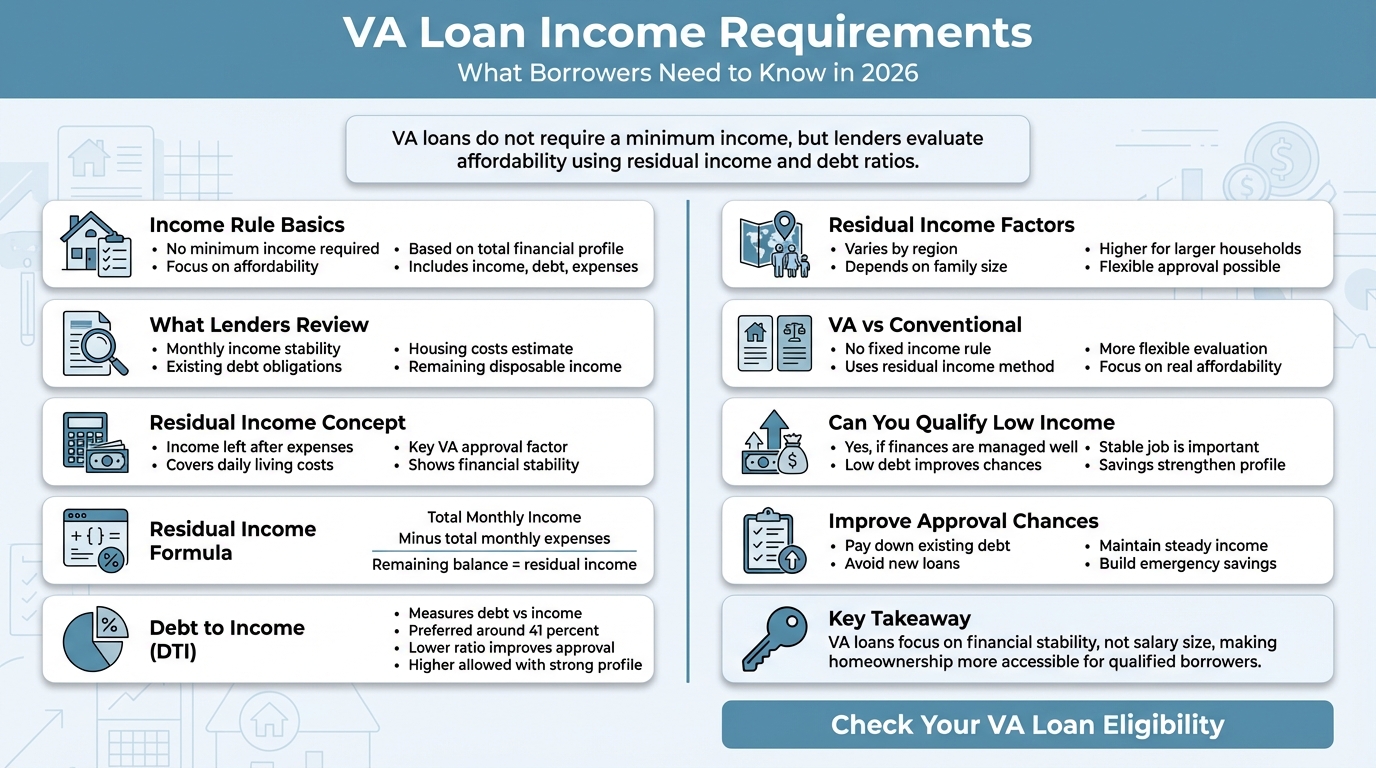

The reality is different. VA loans do not set a fixed minimum income level. Instead, lenders look at how well you can manage your monthly financial obligations after taking on a mortgage.

This approach makes VA loans more flexible and accessible compared to many other loan types. Understanding how income is evaluated will help you prepare and improve your chances of approval.

Do VA Loans Require a Minimum Income?

There is no official income threshold required to qualify for a VA loan. You are not required to earn a specific salary amount to be eligible.

However, lenders still need to confirm that you can comfortably afford your mortgage payments. Instead of focusing on income alone, they evaluate your full financial picture.

This includes:

- Your monthly earnings

- Existing debts

- Estimated housing costs

- Remaining disposable income

The goal is simple. Lenders want to ensure you can handle homeownership without financial strain .

What Is Residual Income and Why It Matters

Residual income is one of the most important concepts in VA lending. It represents the money you have left each month after paying all essential expenses.

These expenses include:

- Mortgage payment

- Loan obligations like car loans or credit cards

- Taxes and insurance

Residual Income Formula

Residual Income = Total Monthly Income minus Total Monthly Expenses

If you still have enough money left after these payments, it shows that you can maintain a stable financial lifestyle.

This is why VA loans rely heavily on residual income instead of setting a minimum salary requirement.

Residual Income Guidelines by Region

Residual income requirements are not the same for everyone. They vary depending on where you live and how many people are in your household.

Below is a simplified reference table for typical requirements.

Residual Income Table

For larger households, the required amount increases slightly for each additional member.

These values are not strict cutoffs. Lenders may still approve applications that fall below these numbers if other financial strengths are present .

Understanding Debt to Income Ratio

Another important factor is your debt to income ratio. This shows how much of your income is used to pay debts.

Example Calculation

Most lenders prefer a ratio around or below 41 percent. A lower ratio indicates that you have more financial flexibility.

Even if your ratio is slightly higher, strong residual income can help balance your application.

VA Loan vs Conventional Loan Income Evaluation

VA loans use a different method compared to conventional mortgages. This difference makes them more borrower friendly.

Comparison Table

This flexible approach is one of the main reasons many eligible borrowers prefer VA loans.

Can You Qualify With a Lower Income

Yes, qualifying with a lower income is possible under the VA loan program. The key is how well you manage your finances.

You may still qualify if you have:

- Low monthly debt

- Stable job history

- Good credit behavior

- Additional savings

Adding a co borrower, such as a spouse, can also strengthen your application by increasing total household income .

How Lenders Evaluate Your Application

VA lenders do not rely on a single number. They review several factors together to make a decision.

Key Evaluation Points

- Income consistency

Steady employment shows reliability - Monthly obligations

Lower debt improves your financial profile - Residual income

Ensures you can handle everyday expenses - Credit history

Indicates how well you manage borrowed money - Cash reserves

Savings provide a safety buffer

This combined review process allows more flexibility than traditional loan approvals.

Practical Ways to Improve Eligibility

Even though there is no minimum income requirement, preparing your finances can improve approval chances.

Tips to Strengthen Your Profile

- Pay down existing debts before applying

- Avoid taking on new loans during the process

- Maintain stable employment

- Build savings for emergencies

- Choose a home within your budget

These steps help improve both your residual income and debt ratio.

Common Misunderstandings About VA Loan Income

You must earn a high salary

Not true. Affordability matters more than income size.

Only military income counts

Incorrect. Household income can be included if applying jointly.

Low residual income means rejection

Not always. Other strengths can offset this factor.

Why VA Loans Use Residual Income

The VA loan program focuses on long term financial stability. Instead of approving loans based only on income, it ensures borrowers can maintain a comfortable lifestyle after buying a home.

This reduces financial stress and helps borrowers avoid default.

By using residual income, lenders can better understand real life affordability.

Conclusion

VA loans do not require a minimum income, but they do require responsible financial management. Residual income and debt to income ratio are the key factors that determine eligibility.

Borrowers who maintain stable finances, manage debt carefully, and plan their home purchase wisely can successfully qualify for a VA loan in 2026.

FAQs

1. Do VA loans require a minimum income level

No, there is no fixed income requirement. Lenders focus on affordability through residual income and overall financial stability.

2. What is considered good residual income

It depends on your region and family size. Meeting or exceeding guideline levels improves your chances of approval.

3. Can I get approved with high debt

It is possible, but a lower debt to income ratio is preferred. Strong residual income can help offset higher debt levels.

4. Does my spouse income count

Yes, if your spouse is a co borrower, their income is included in the total household income.

5. What improves VA loan approval chances

Stable income, low debt, good credit, and sufficient residual income all increase approval likelihood.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)