.avif)

VA Break Even Analysis in California: Choosing Between Upfront Cost and Long Term Interest Savings

Refinancing a VA loan in California often involves a trade off between paying upfront costs and securing long term interest savings. The concept of break even analysis helps borrowers determine whether the refinance actually makes financial sense over time.

A VA refinance can reduce your interest rate, change your loan term, or improve cash flow. However, closing costs and fees must be weighed against monthly savings. Understanding how to calculate and interpret break even is essential before moving forward.

What Is VA Break Even Analysis

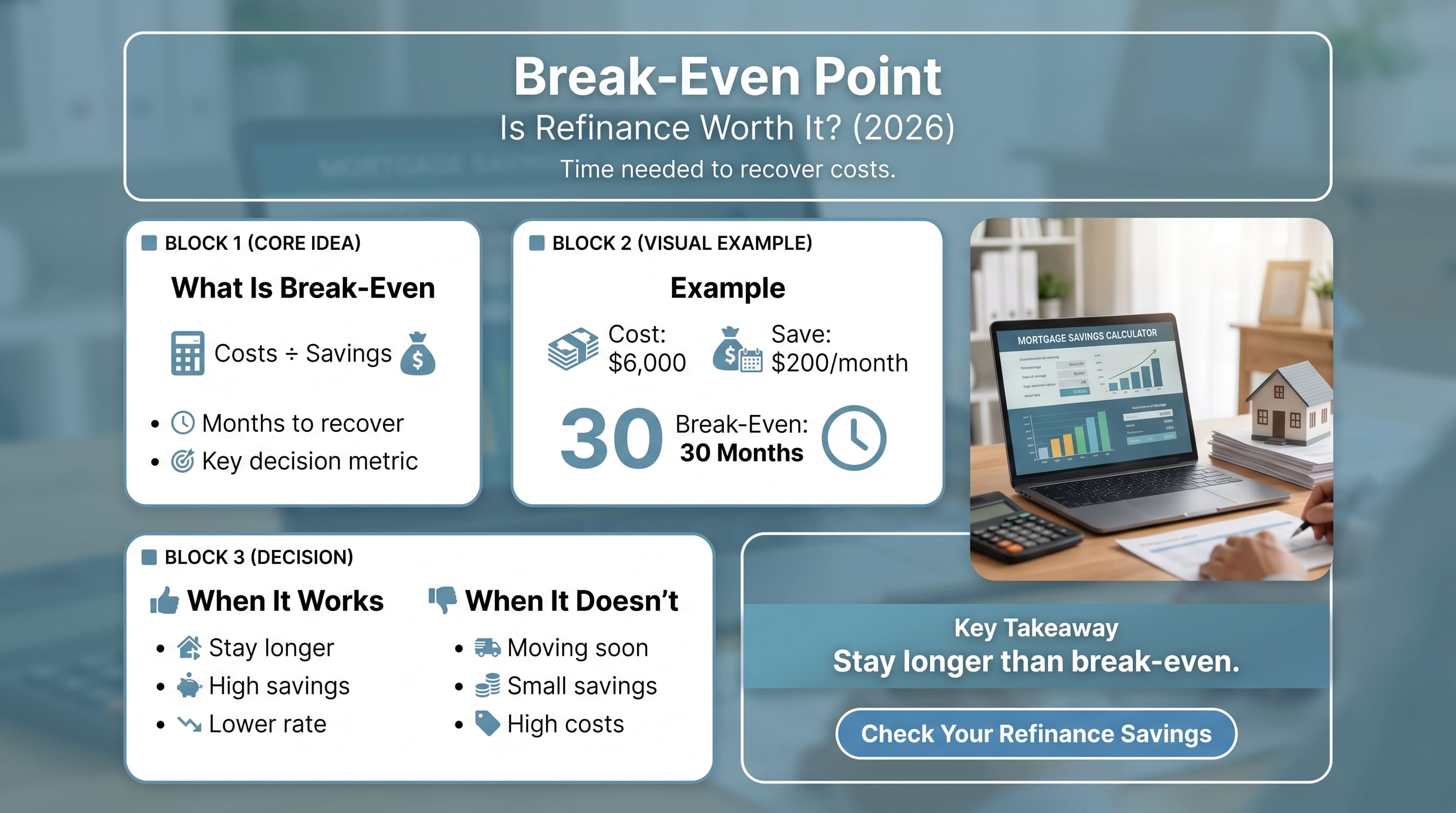

VA break even analysis measures how long it takes for your monthly savings from refinancing to recover the upfront costs you paid to obtain the new loan.

Basic Concept

Break even point equals total closing costs divided by monthly savings

This calculation shows how many months it will take to offset the cost of refinancing.

Why Break Even Matters in California

California borrowers often deal with higher loan balances and closing costs. Because of this:

- Savings can be significant but costs are also higher

- Break even timelines can vary widely

- Market conditions influence rate differences

A refinance that looks beneficial on the surface may not make sense if the break even period is too long.

Key Components of Break Even Analysis

Several factors influence the break even calculation.

Closing Costs

- Lender fees

- Title and escrow charges

- VA funding fee if applicable

Monthly Savings

- Reduction in interest rate

- Lower monthly payment

- Term adjustment impact

Loan Term

- Extending the term can reduce payment but increase total interest

- Shortening the term increases payment but reduces long term cost

Example Calculation

Consider a borrower in California:

- Closing costs: 6000

- Monthly savings: 200

Break even point:

- 6000 divided by 200 equals 30 months

This means the borrower must stay in the loan for at least 30 months to recover costs.

Short Term vs Long Term Strategy

California Market Considerations

In California:

- Higher property values lead to larger loan amounts

- Even small rate reductions can create meaningful savings

- Closing costs are often higher due to transaction size

Because of this, break even analysis becomes more important compared to lower cost markets.

When Break Even Favors Refinancing

Refinancing makes sense when:

- You plan to stay in the home beyond the break even period

- Monthly savings are significant

- Interest rate reduction is meaningful

- Long term cost reduction is clear

When Break Even Does Not Work

Refinancing may not be ideal when:

- Break even period is too long

- You plan to move or sell soon

- Savings are minimal

- Costs outweigh benefits

Risk Factors to Consider

Common Borrower Mistakes

Many borrowers misunderstand break even analysis.

Common issues include:

- Focusing only on monthly savings

- Ignoring total cost of refinance

- Not considering time horizon

- Overlooking long term interest impact

How to Evaluate Your Break Even Point

A structured approach helps:

- Calculate total upfront costs

- Estimate realistic monthly savings

- Determine how long you plan to stay in the home

- Compare multiple refinance options

This ensures better decision making.

Strategic Perspective

In California, VA break even analysis is often used to:

- Decide between rate reduction and cost

- Evaluate refinancing timing

- Optimize long term savings

Understanding this concept allows borrowers to use refinancing as a financial strategy rather than just a rate adjustment.

Final Thoughts

VA break even analysis helps borrowers balance upfront costs with long term savings. In California, where loan sizes are larger, this calculation becomes even more important.

Choosing the right refinance option depends on how long you plan to stay in the home and how much you value monthly savings versus long term interest reduction.

This analysis is based on lending experience and borrower refinancing patterns observed by Bill Marshall. For structured VA refinance guidance and California mortgage strategies, Merchants Home Lending provides professional support aligned with current lending practices.

FAQs

What is VA break even analysis

It is the time required to recover refinance costs through monthly savings.

How do you calculate break even

Divide total closing costs by monthly savings.

Is shorter break even better

Yes, it means you recover costs faster.

Should I refinance if break even is long

Only if you plan to stay in the home long enough to recover costs.

Does break even include interest savings

It focuses on monthly savings but should be combined with total interest analysis.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)