.avif)

VA Guaranty in California: How It Protects Lenders and Helps Veterans Buy With Zero Down

Veterans in California often rely on VA loan benefits to access homeownership with favorable terms. One of the most important components behind this program is the va guaranty. It plays a critical role in reducing lender risk while allowing eligible borrowers to purchase homes with little to no down payment.

Understanding how a va guaranty loan works helps borrowers see why lenders are willing to offer flexible terms that are not typically available with conventional financing.

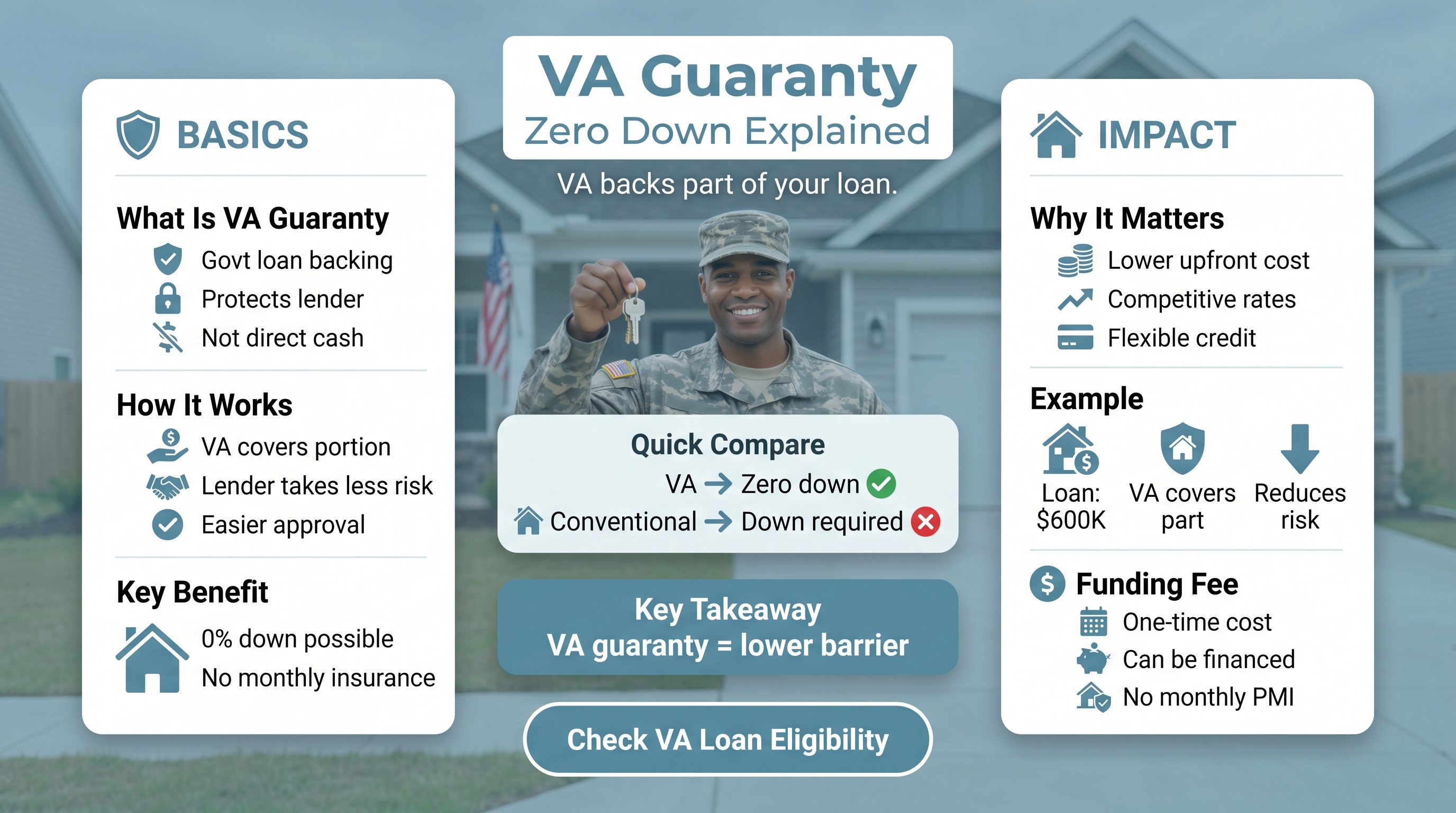

What Is VA Guaranty

The va guaranty is a financial backing provided by the Department of Veterans Affairs to approved lenders. It guarantees a portion of the loan amount in case the borrower defaults.

This guarantee does not go directly to the borrower. Instead, it protects the lender, which allows them to offer:

- Zero down payment options

- Competitive interest rates

- Flexible credit requirements

Because of this structure, a va guaranty loan becomes one of the most accessible home financing options for eligible veterans.

How VA Guaranty Works

The va guaranty typically covers a percentage of the loan amount. If a borrower defaults, the VA reimburses the lender for the guaranteed portion.

Key Points

- The guaranty reduces lender risk

- It replaces the need for private mortgage insurance

- It supports higher loan approval flexibility

This system is what enables zero down financing in most cases.

VA Guaranty Loan Structure

VA Guaranty in California Market

California has high property values in many regions, which makes down payments a major barrier for buyers.

The va guaranty loan helps overcome this challenge by:

- Eliminating large upfront cash requirements

- Allowing veterans to enter competitive markets

- Supporting affordability despite higher home prices

Because of this, VA loans are widely used across California.

VA Guaranty Calculator Concept

A va guaranty calculator helps estimate how much of the loan is covered by the VA.

While exact calculations depend on loan size and entitlement, the general idea is:

- VA guarantees a portion of the loan

- Remaining portion is lender exposure

Understanding this breakdown helps borrowers see how lenders evaluate risk.

Example Scenario

Consider a California home purchase:

- Loan amount: 600000

- VA guaranty covers a portion of this amount

If default occurs:

- VA pays the guaranteed portion

- Lender absorbs remaining risk

This is why lenders are more flexible with va guaranty loan approvals.

VA Guaranty Fee Explained

The va guaranty fee, also known as the funding fee, is a one time charge paid by the borrower.

Key Features

- Helps sustain the VA loan program

- Can be financed into the loan

- Varies based on usage and down payment

This fee replaces monthly mortgage insurance costs found in other loan types.

VA Loan vs Conventional Loan

Benefits of VA Guaranty for Borrowers

The va guaranty provides several advantages:

- Reduced upfront costs

- No monthly mortgage insurance

- Easier qualification standards

- Access to competitive loan terms

These benefits make VA loans a strong option in high cost markets like California.

Benefits for Lenders

From a lender perspective, the va guaranty loan offers:

- Risk reduction

- Higher approval confidence

- Stable loan performance

This creates a balanced system where both borrower and lender benefit.

Risk Factors to Consider

Understanding these risks helps borrowers make informed decisions.

Common Misunderstandings

Many borrowers misunderstand how va guaranty works.

Common misconceptions include:

- VA gives money directly to the borrower

- The loan is fully guaranteed

- No repayment responsibility exists

In reality, the guaranty protects the lender, not the borrower.

How to Use VA Guaranty Strategically

A structured approach improves outcomes:

- Confirm eligibility and entitlement

- Understand guaranty coverage

- Evaluate long term affordability

- Compare with other loan options

This ensures the va guaranty loan is used effectively.

California Strategy Perspective

In California, where affordability is a major concern, VA loans provide a significant advantage.

- Zero down helps entry into expensive markets

- No mortgage insurance reduces monthly cost

- Guaranty improves approval chances

This makes VA loans a valuable tool for eligible buyers.

Final Thoughts

The va guaranty is the foundation of the VA loan program. It protects lenders while enabling veterans to purchase homes with minimal upfront cost.

Understanding how the va guaranty loan, va guaranty calculator, and va guaranty fee work together allows borrowers to make informed decisions in California’s competitive housing market.

This analysis is based on lending experience and borrower scenarios observed by Bill Marshall. For structured VA loan guidance and California mortgage strategies, Merchants Home Lending provides professional support aligned with current lending practices.

FAQs

What is va guaranty

Va guaranty is a government backed promise that covers a portion of the loan if the borrower defaults.

How does va guaranty loan work

It allows lenders to offer better terms by reducing their risk through partial loan coverage.

What is va guaranty calculator

It is a tool used to estimate how much of the loan is backed by the VA.

What is va guaranty fee

It is a one time funding fee that supports the VA loan program.

Does va guaranty mean no risk

No, it reduces lender risk but does not eliminate borrower responsibility.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)