.avif)

VA Cash Out LTV California Breakdown: How Much You Can Refinance Based on Home Value

Refinancing through a VA program in California can unlock significant home equity, especially in markets where property values have increased over time. One of the most important factors in this process is va cash out ltv, which determines how much of your home’s value you can access.

For veterans, understanding how loan to value works in a VA cash out refinance is critical. It directly affects approval, available cash, and long term loan structure.

What Is VA Cash Out LTV

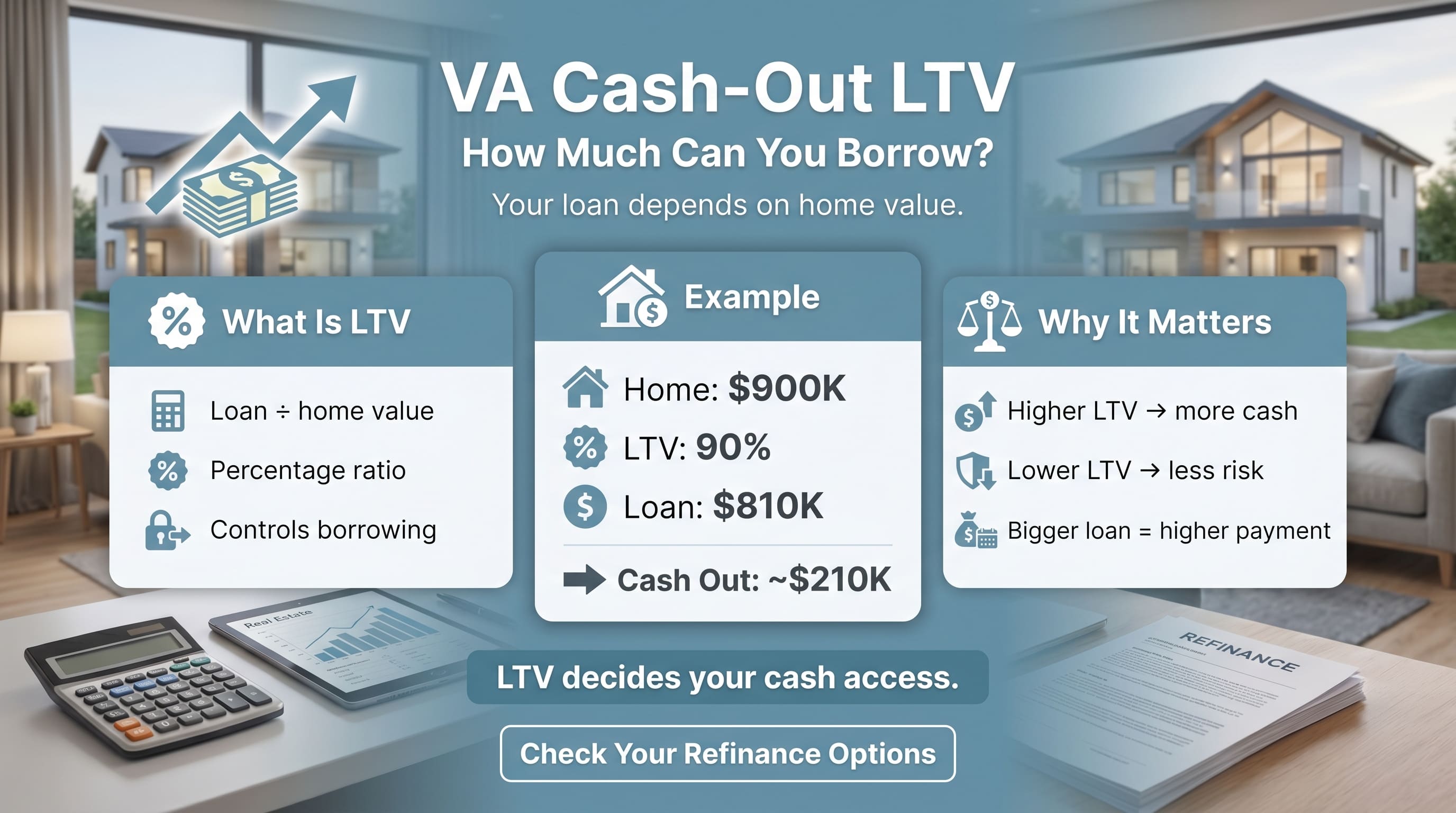

Va cash out ltv stands for loan to value ratio in a VA cash out refinance. It represents the percentage of your home’s appraised value that you can borrow.

Basic Formula

Loan to Value equals Loan Amount divided by Appraised Value

For example:

- Home value: 800000

- Loan amount: 640000

- LTV: 80 percent

In a VA cash out refinance, this ratio determines how much equity you can convert into cash.

Maximum VA Cash Out LTV in California

VA loans are known for allowing higher LTV compared to conventional loans.

Typical guidelines:

- Up to 90 percent LTV is common in many cases

- Some lenders may allow higher levels depending on profile

- Full entitlement borrowers may access higher limits

However, lender overlays and market conditions in California can influence final approval limits.

Comparison Table: VA vs Conventional Cash Out LTV

This makes va cash out ltv one of the most competitive options for accessing equity.

How Home Value Affects LTV

The appraised value of your home plays a major role in determining va cash out ltv.

Higher home value:

- Increases available borrowing capacity

- Improves equity position

- Supports larger cash out amounts

Lower appraisal:

- Reduces available loan amount

- Limits refinancing options

This is why appraisal accuracy is critical in California markets.

Practical Example

A homeowner in California wants to refinance.

Scenario

- Home value: 900000

- Desired LTV: 90 percent

Calculation

- Maximum loan amount: 810000

If the current loan balance is 600000:

- Available cash out: 210000

This example shows how va cash out ltv determines available equity.

Factors That Influence VA Cash Out LTV

Lenders evaluate several elements before approving the loan.

Key Factors

- Credit profile

- Income stability

- Debt obligations

- Property type

- Loan size

Even though VA guidelines allow higher LTV, lender requirements still apply.

Risk Considerations

Borrowers should balance cash access with long term financial stability.

California Market Context

California’s high property values make va cash out ltv especially powerful.

- Significant equity gains in many regions

- Strong refinancing demand

- Competitive lending environment

However, higher loan amounts also require careful financial planning.

When VA Cash Out Refinance Makes Sense

A VA cash out refinance may be beneficial when:

- You need funds for home improvements

- You want to consolidate higher interest debt

- You are restructuring your mortgage

- You have built substantial equity

The key is ensuring the new loan aligns with long term goals.

Common Borrower Mistakes

Many borrowers misunderstand va cash out ltv.

Common issues include:

- Borrowing maximum amount without planning

- Ignoring long term repayment impact

- Overestimating property value

- Not comparing lender options

Avoiding these mistakes improves financial outcomes.

How to Evaluate Your LTV Position

Before refinancing, borrowers should:

- Estimate current home value

- Calculate existing loan balance

- Determine target LTV

- Review lender guidelines

This helps create a realistic refinancing strategy.

Strategic Perspective

In California, VA cash out refinancing is often used as a financial tool rather than just a loan adjustment.

- Accessing equity for investments

- Managing debt efficiently

- Leveraging property appreciation

Understanding va cash out ltv ensures this strategy is used effectively.

Final Thoughts

The va cash out ltv determines how much of your home’s value you can access through refinancing. In California, where property values are often high, this can provide significant financial flexibility.

However, higher LTV also means increased loan size and long term commitment. Borrowers should carefully evaluate their financial goals before proceeding.

This analysis is based on lending experience and borrower refinancing patterns observed by Bill Marshall. For structured VA refinance guidance and California mortgage strategies, Merchants Home Lending provides professional support aligned with current lending practices.

FAQs

What is va cash out ltv

It is the percentage of your home value you can borrow in a VA cash out refinance.

What is maximum va cash out ltv

It can go up to high levels depending on lender guidelines and borrower profile.

Does higher ltv mean more cash

Yes, a higher LTV allows more borrowing against home equity.

Is va cash out better than conventional

It often allows higher LTV and more flexibility.

Does appraisal affect va cash out ltv

Yes, the appraised value directly impacts how much you can borrow.

Check VA Rates Now

Take a first step towards your dream home

Free & non binding

No documents required

No impact on credit score

No hidden costs

.svg)

.svg)